Two Identical Stacks, Two Different Premiums

Two companies can run the exact same stack. Same MFA product, same backup software, same EDR. They can land on completely different premiums, because one of them can hand an underwriter evidence, and the other can only hand them a policy document.

Your premium isn't based only on the security tools you bought. It's also based on how convincingly you can demonstrate they reduce risk.

Your renewal was not decided this year. It was decided two years ago, when you picked the vendors and built the architecture your environment still runs on today. This year, that decision priced out at 15 to 20% higher.

You're Asking the Wrong Question

The renewal conversation puts one question in front of you: what do I need to buy or fix right now to bring this number down?

That's the vendor framed version. Every broker, every MSP, and every security vendor selling into this cycle has an answer ready, because the answer is usually their product.

The real question is different. Which of the decisions you made years ago is an underwriter actually scoring today, and can you prove it, or only assert it?

What the Underwriter Is Actually Scoring

Five years ago, a cyber insurance application was a short questionnaire and a signature. Carriers took your word for it.

That's gone. Several major carriers now run external attack surface scans and request evidence directly: screenshots, exports from your RMM or PSA platform, third party verification, before an underwriter ever finishes reading your application.

MFA and EDR are among the controls carriers scrutinize most closely, and missing either frequently results in higher premiums, coverage restrictions, or an outright decline. Every carrier weighs its own mix, some lean harder on privileged access, email security, or business continuity, but MFA and EDR show up as gating requirements more than almost anything else on the application.

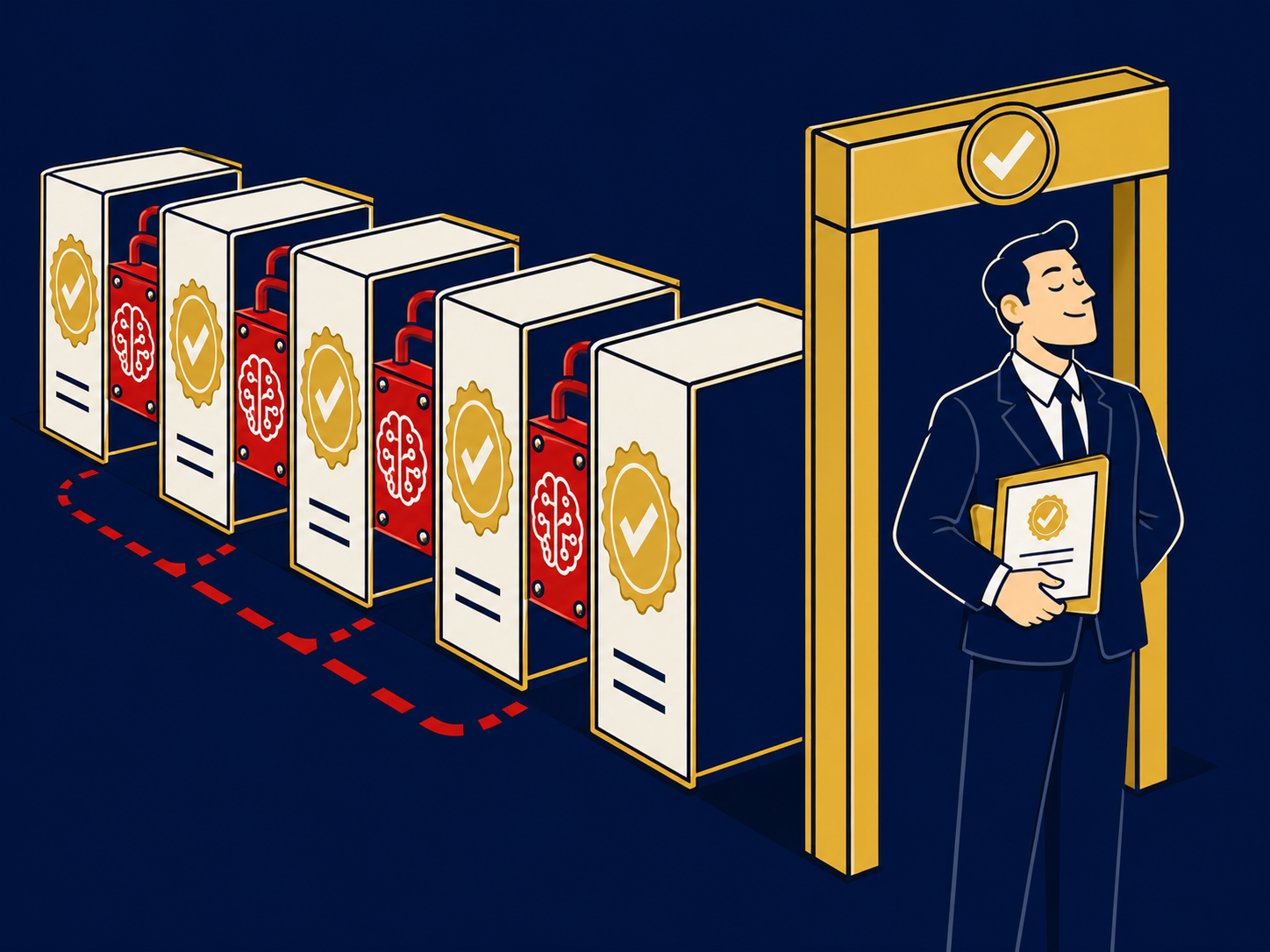

The Gap Between "Installed" and "Proven"

This is where the evidence gap actually shows up. In every pair below, the underlying control was identical. Only the proof changed.

MFA. Weak evidence is a policy sitting in a folder. Strong evidence is an enforcement report showing MFA active on every privileged account.

Backups. Weak evidence is backup software installed. Strong evidence is a documented, dated, successful restore test.

Patching. Weak evidence is a written patch policy. Strong evidence is patch compliance evidence with timestamps.

Incident response. Weak evidence is a written incident response plan. Strong evidence is tabletop exercise records or documented testing.

That's what the underwriter is actually scoring: not whether the control exists, but whether you can hand over proof of it on request.

Why Some Purchases Do Nothing for Your Renewal

Swap your MDR vendor for a newer one, and a carrier will often price you exactly the same. Brand was never what they were scoring.

The technology decisions that most affect how underwriters assess your risk are usually the hardest to change before renewal and they're rarely the ones a broker brings up:

- A flat network you built five years ago

- Identity architecture that never separated privileged access from standard accounts

- A legacy VPN nobody replaced because migrating it would touch too many systems at once

- Unsupported operating systems still running something the business depends on

None of those get fixed with a purchase order before your next renewal. They get fixed with a roadmap. The earlier you know they're the reason your premium is high, the earlier that roadmap can start.

What to Check Before Your Next Renewal Call

Stop asking whether you have MFA. Start asking whether you can produce the enforcement report for every privileged account, not just the ones your original rollout covered.

Ask whether your last backup test was a documented restore, not a completed backup job.

Ask whether your patch compliance has timestamps and tickets behind it, or a policy nobody has opened since it was written.

Ask which parts of your architecture, not your tool list, would take longer than a renewal cycle to change, even if you decided today.

If you can't answer these with evidence in hand, you already know what the scan is going to find before your broker does.

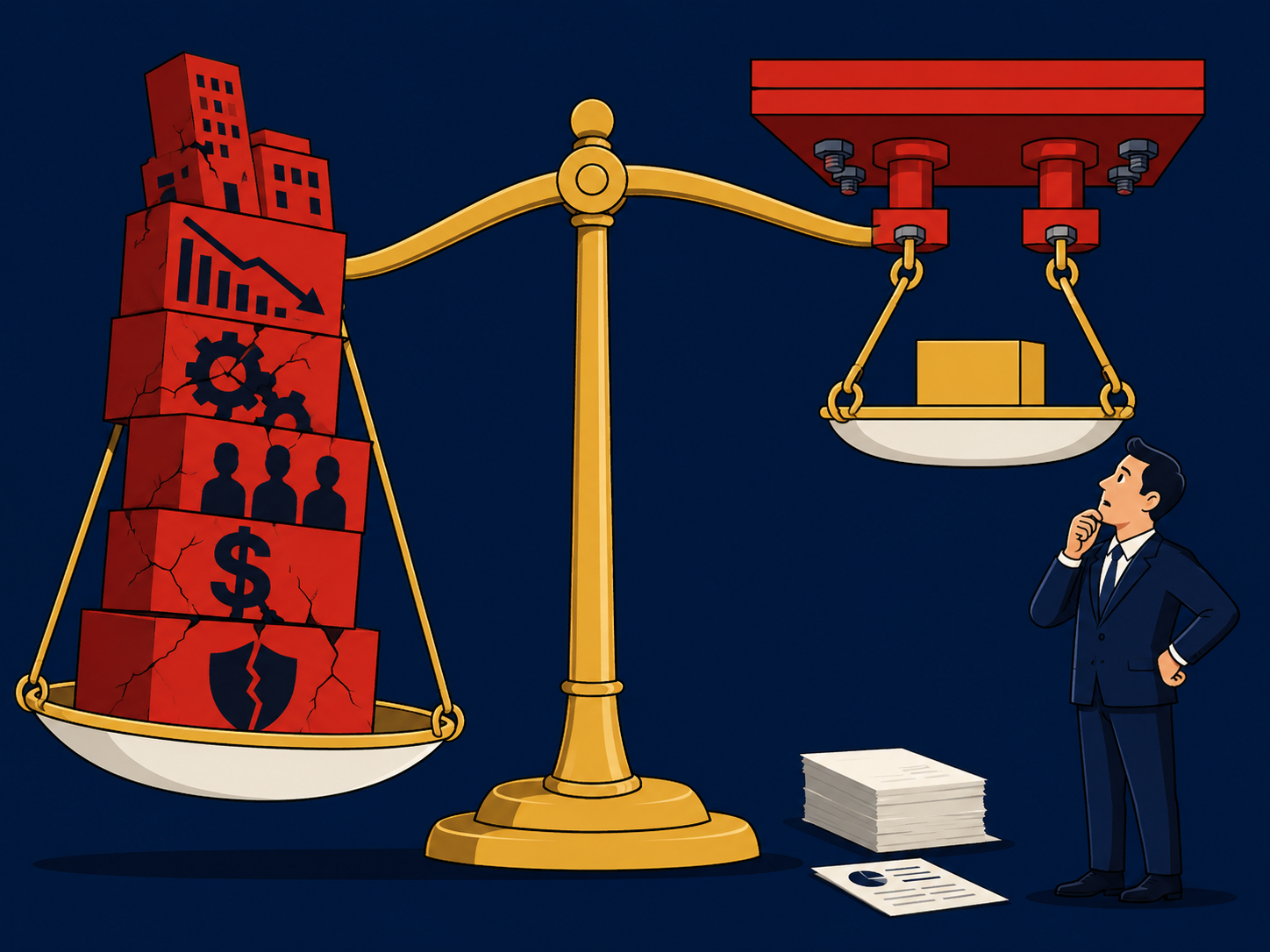

The Number Behind the Number

Seventy percent of companies reported higher costs on this year's renewals. The spread between what two similar companies pay for the same coverage can run 30 to 50%, driven not only by the underlying risk, but by how well that risk can be evidenced and explained during underwriting.

For a typical mid market company, the difference between weak and documented controls can move a $20,000 premium down to $13,000 to $15,000. Nobody decides that gap in the renewal meeting. It gets decided by whether the proof existed before anyone asked for it.

If This Is Where You Are Right Now

If your last renewal came in higher than expected, or you're not certain your team could produce evidence, not policy, for MFA, backups, and patching on request today, this applies to you now. Not at your next renewal date.

Before your broker tells you what to buy, find out what your underwriter is actually scoring. That's what changes once someone independent is checking your stack against what underwriters score, not what vendors sell.

See what an underwriter is likely to score before your renewal.

Get Started. No pitch. No prep. Just answers.